Why Risk Management Is Important for Growth and How Alternatives Can Help

As Benjamin Graham, one of the investing world’s original greats, said, “The essence of investment management is the management of risks, not the management of returns.” Regrettably, too many investors worry about the risks when it’s too late. As I have heard too often: “I want to be aggressive, but only when the market is going up!”

Of course, that’s what we all want; the problem is that no one knows when the market is going to go up and when it’s going to go down. If we did, investing would be a lot easier!

While stocks offer growth potential, they’re volatile. To free yourself from risk, you need to put your money in a savings account, and we all know what such accounts are paying these days. In order to keep up with inflation, or to grow your investments above inflation, you need to take risk. Consider, however, that a 50% decline in your portfolio requires a 100% gain to break even. Volatility reduces long-term growth and should be reduced as much as possible.

Volatility

From a mathematical perspective, volatility is harmful to growth because it acts as an anchor on compounding returns. Look at two hypothetical USD 1 million portfolios that have average annual returns of 8% for the 10-year period (Figure 1). While the average returns were the same, the portfolio with lower volatility grew by nearly 10% more.

Figure 1. Volatility effects on a portfolio.

The drag on growth can be estimated with a formula, but I won’t bore you with the math here. Suffice it to say that volatility is not a friend to growing your assets.

Emotional Risk

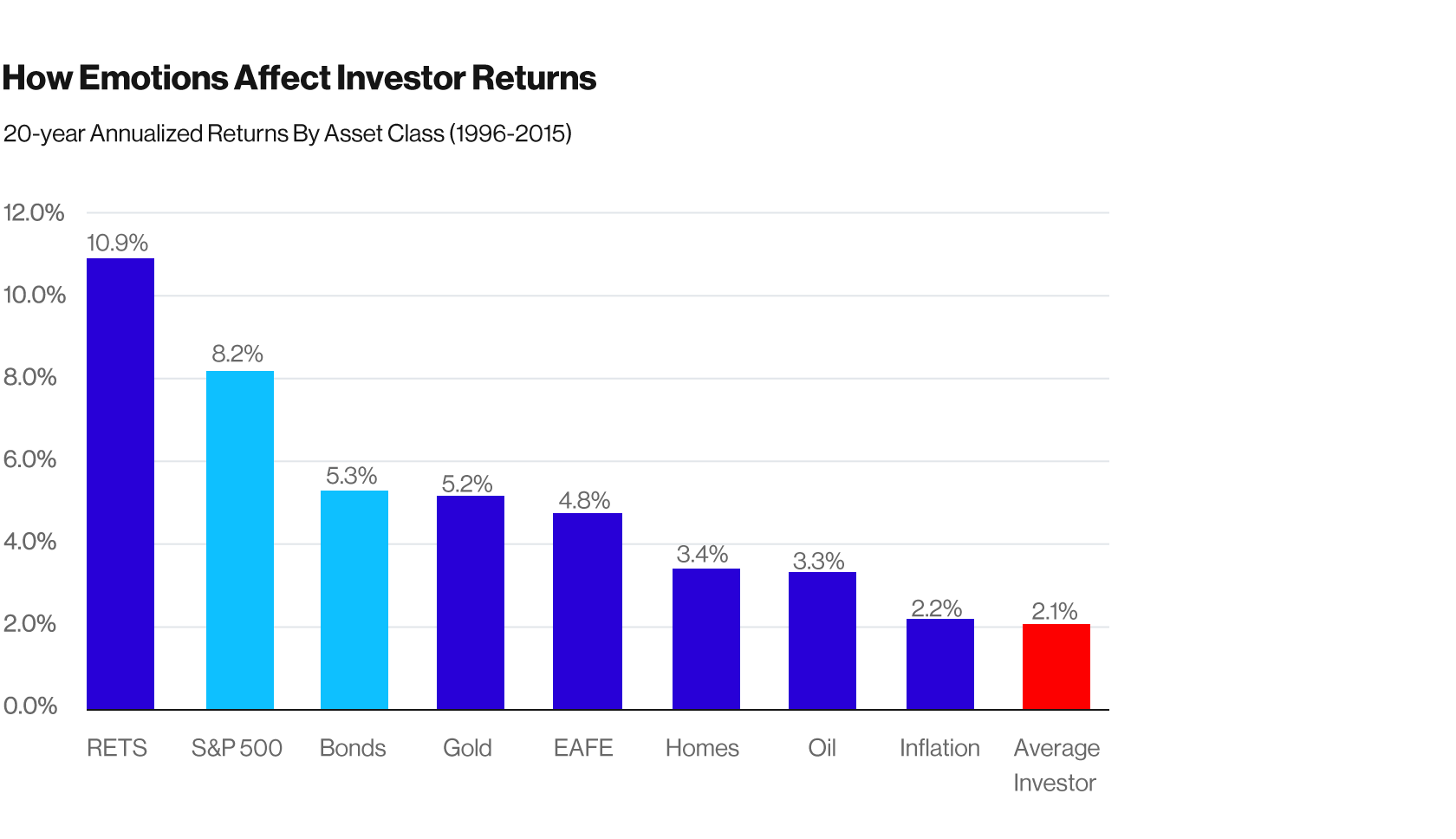

The second problem with volatility is its effect on emotions. Numerous behavioral finance studies show how emotions play havoc with investment decisions and force investors to jump in and out of the market at the wrong time. As a result, realized returns suffer. Table 1 quantifies this effect and illustrates how poorly the average investor does by realizing returns well below the returns of stocks and bonds.

Table 1. How Emotions Affect Investor Returns

Therefore, risk management, or the reduction in volatility, is important. You need to make sure that when taking risk, you are compensated for that risk.

What does this mean? Simply put, diversify and always remain diversified. Make sure the sources of returns in your portfolio are varied. Holding a basket of stocks is better than holding one stock or “putting your eggs in one basket.” Additionally, holding assets other than stocks further diversifies your portfolio, since stocks tend to rise and fall together.

Bonds and Alternatives

This is where bonds and alternatives come into play. Since many of these assets do not move in tandem with stocks, they can broaden the diversification and improve the return for the level of risk. Because returns for asset classes differ from year to year, there will be times when these assets add to growth and times when they detract, but as a risk management tool, they are vital.

Plenty of investors have been investing in bonds to lower risk for quite some time; however, for most investors, alternatives have only been around for a shorter period.

Since the performance of many alternatives is not tied to the performance of stocks or bonds, they can reduce volatility without lowering returns. To be sure, all alternatives are not alike, and some are more correlated or reliant on the movement of stocks and bonds than others.

Table 2. illustrates the differences in some of the more commonly used risk-reduction alternative strategies. It should be clear that while alternatives are different from the usual equity and fixed income asset classes, they are not homogeneous and have very diverse characteristics. In addition, although we generally refer to them as alternative assets, it is more accurate to call them alternative strategies because many of the strategies still use stocks or bonds—they just manage them differently.

Table 2. Risk-Reduction Alternatives and Their Returns

*Sources for this data are the following indices obtained via Morningstar Direct: Credit Suisse Long/Short Equity, Credit Suisse Market Neutral, Credit Suisse Global Macro, Credit Suisse Managed Futures, and the Bloomberg Barclay's US Aggregate Bond.

Long/short equity strategies invest in the stock market and generally move in the same positive or negative direction as the equity market, but with less volatility.

Market neutral strategies involve going both long and short stocks in equal amounts so your return is principally due to the manager’s ability to buy stocks that will increase in value and short stocks that will lose value, not by the movement in the market.

Global macro strategies focus on global economies and profit by investing in assets whose prices are most directly influenced by macro events. Consequently, they participate in all major markets: bonds, currencies, commodities, and equities.

Managed futures describes the category of alternative strategies that specialize in using the global futures markets. In place of stocks and bonds, managers invest in futures contracts and most try to capitalize on trends.

While Table 2 highlights common hedge funds used to reduce risk, alternatives also include investments to hedge against inflation. These strategies, called real return strategies, have a higher correlation to the movements in the price index (inflation) than common stocks, providing inflation protection. These strategies include: commodities, real estate, and infrastructure investing. Commodities and commercial real estate tend to rise with the level of inflation and, as a result, offer inflation protection despite the added volatility.

Infrastructure investing is basically investing in the base upon which economic growth is built. This base includes a country or community's roads, utilities, water, sewage, etc. Infrastructure investments share attributes of private equity, real estate, and fixed income.

Increasing Opportunities

While alternatives can improve risk-adjusted returns, their availability has historically been limited. With the advent of more liquid investments, like mutual funds and exchange-traded funds (ETFs), alternative investments can add value to a much larger group of investors. Similar to the way stock and bond mutual funds expanded the ability of smaller investors to invest in the markets, so too can alternative mutual funds. There is a caveat, though: while adding alternatives can lower risk, because of their complexity and differences, proper due diligence is needed before investing.

About the Author

Richard Cloutier, CFA, is the chief investment strategist for Washington Trust Bank. He has more than 20 years investment experience. Rick has written numerous articles for Investopedia and wrote a weekly column for the Fall River Herald News in Massachusetts. His research has appeared in the Journal of Investment Management and Financial Innovations, as well as the International Journal of Revenue Management. He provided a nightly commentary on WALE radio and authored the novel Caveat Emptor. Rick earned his MBA at Boston University.